Small Business Equipment Loans

Equipment loans can provide the necessary capital to purchase tools and machinery to grow your business. We designed our product to meet the needs of small businesses with flexible repayment terms and competitive interest rates. At Camino financial, we can provide the financial aid you need to purchase the equipment you need to run your business effectively.The Benefits of Getting a Business Loan to Buy Equipment

Using a business loan to buy equipment offers numerous advantages, including the immediate acquisition of vital assets without depleting cash reserves, enabling businesses to maintain liquidity for operational needs and emergencies.

This approach also allows companies to take advantage of the latest technology and equipment, thereby staying competitive and efficient.

Our Business Equipment Loans

Varied loan amounts

Fixed

Interest rates

Repayment terms

Why Apply for Our Equipment Financing

Upgrading to new equipment boosts productivity and quality, yielding customer satisfaction and cost savings due to improved efficiency and reduced repairs. It can also give you a competitive edge and increase employee satisfaction, potentially lowering turnover. Our small business equipment loans can help you buy the necessary tools or machinery to take your business to the next level. The best part is that we don't require you to put up the equipment you're buying as collateral.Our Basic Business Loan Application Requirements

✓ Have an SSN

✓ Minimum credit score of 670

✓ Business in operation for a minimum of 12 months

✓ Annual sales above $30,000

✓ Current on outstanding credit obligations

✓ No filed tax liens, judgments, credit freezes, or bankruptcies in the past 24 months

✓ Must operate within permitted industries and states

Should You Get an Equipment Loan or Lease Equipment?

Equipment Loan Equipment Leasing Ownership You own the equipment outright once the loan is paid off. You do not own the equipment and must return it at the end of the lease term unless there's an option to buy. Flexibility Loans offer less flexibility to upgrade, but this is balanced by the advantage of ownership and potential for longer-term use without the need to upgrade. Leasing offers the ability to upgrade to newer equipment more frequently, beneficial for technology that becomes outdated quickly. End of Term At the end of the loan term, there are no further obligations; the equipment is yours. At the end of the lease, you may have options: return the equipment, renew the lease, or buy the equipment at market value. Interest Rates and Total Cost Owning the equipment can be more cost-effective over time. The overall cost can be higher over the long term due to continuous leasing. Suitability Ideal for businesses looking to invest in long-term assets and build equity. Best for businesses that need to keep up with the latest equipment without the burden of ownership. When Is the Right Moment to Finance Equipment?

ExansionTechnologyLiquidityNecessityProfitabilityAffordabilityWhen Expansion is in Sight

If your business is scaling up and you need additional equipment to support growth, financing can help you acquire necessary assets without depleting your cash reserves.

Why Choose Camino Financial

● A completely digital application experience ● Fixed terms with competitive rates ● Your security and privacy are our top priorities ● We have no penalties for early loan repayment ● Our customer service team is bilingual ● We have no hidden processing feedRead What Others Are Saying

Join 9,000+ people choosing Camino Financial

Anthony Williams

“This was the best loan application experience ever. Other financial institutions need to take a look at how Camino delivers and operates...”Bernie Bravo

“...Camino Financial was great to work with and I love how they determined the loan amount based on my personal guarantee.”Rubert Velasquez

“...Camino is the best I’ve encountered so far. They’re always there to help and really make things happen in a professional, timely manner. Thanks Yvette!”What Kind of Equipment Can You Finance?

1

Office equipment

This includes computers, printers, copiers, office furniture, and telecommunications systems essential for day-to-day operations.

2

Technology and software

Advanced software, IT hardware, servers, and network infrastructure can be quite costly and are often financed to keep up with the latest technology.

3

Heavy machinery

This category includes construction equipment like excavators, bulldozers, cranes, and backhoes, vital for construction companies and contractors.

4

Production and manufacturing tools

General machinery and tools used in the creation, assembly, and packaging of products, adaptable to different production needs.

5

Vehicles and transportation

Company cars, delivery vans, trucks, and trailers used for logistics, delivery services, and employee transportation.

6

Retail and point of sale (POS) systems

Cash registers, inventory management systems, and display units are essential for retail operations.

7

Food service equipment

Appliances and tools required for food preparation, storage, and service in restaurants and catering services.

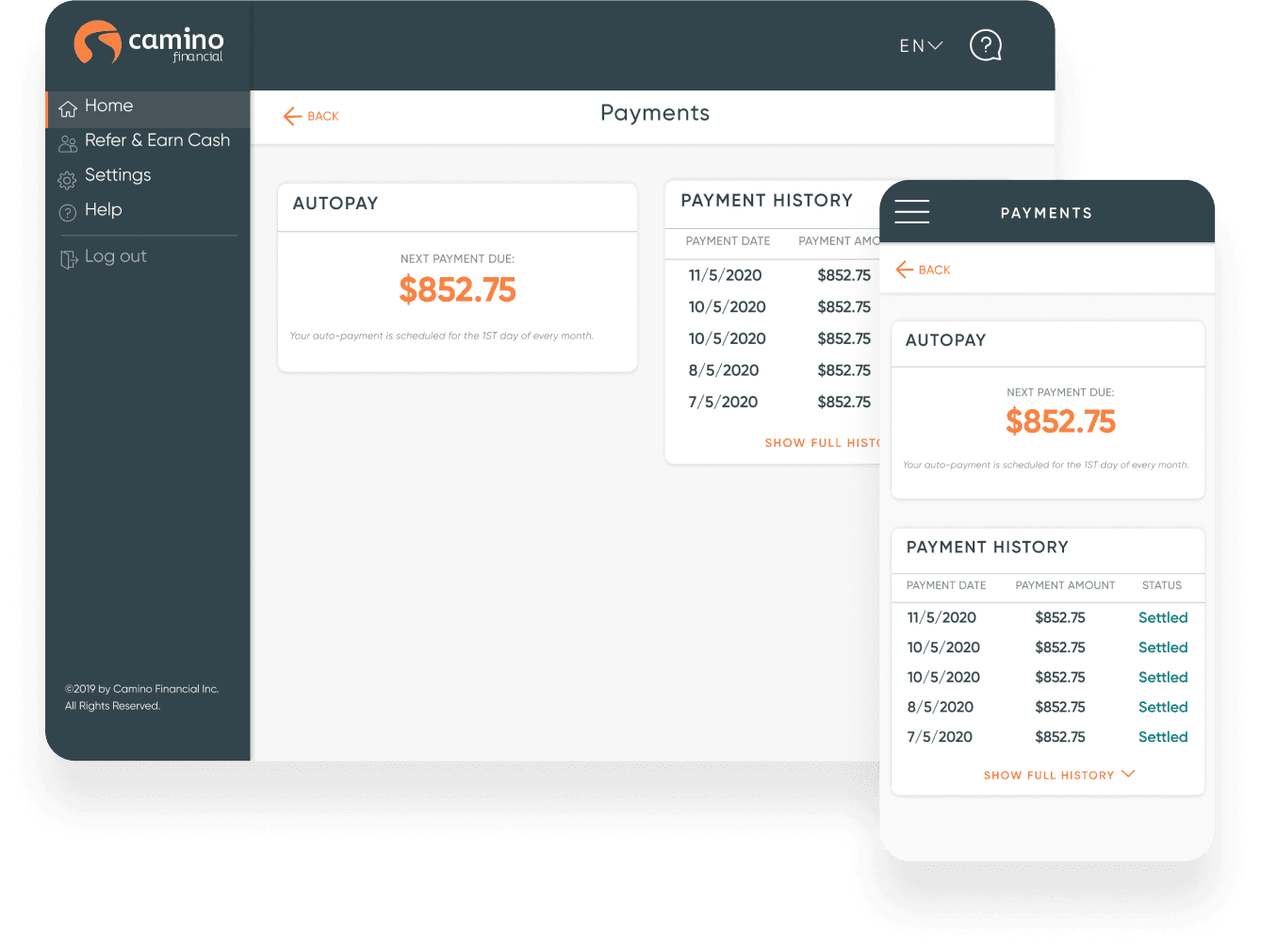

Discover Camino Financial's convenient loan management

Get a visual overview of loan status. Track payment history and request more capital through your personalized member account portal.How To Get Equipment Financing With Camino Financial

FAQs

To finance new equipment. If a small business grows or expands, it may need to buy new equipment to keep up with demand. This could include anything from computers and software to machinery.

To renovate or upgrade existing equipment. If a small business's machinery is old or outdated, you may need to renovate or upgrade it. This could include anything from replacing outdated computers with new ones to adding new features to existing equipment.

To cover unexpected expenses. If a small business experiences an unexpected expense, such as a natural disaster or a theft, it may need to take out a loan to cover the costs. This could include replacing damaged equipment.Equipment financing is a business loan to purchase new or used machinery. A lease is a contract between a business and a leasing company that allows the business to use the machinery for some time without owning it.

Yes. As a BBB-accredited business with an A+ rating and an average of 4.2 stars across more than 400 reviews prove it.

Camino Financial uses the same technology that banks use to protect your private information.

Have a Social Security Number (ITIN is not accepted).

Business must have been operational for at least 12 months.

A credit score of 670 or higher is required.

Specialty Trade Contractors with a FICO score of 650 or above.

Must have annual sales exceeding $30,000

Must be up-to-date on all existing credit responsibilities.

No record of tax liens, judgments, credit .freezes, or bankruptcies in the last 24 months

Not operating in prohibited sectors.

No businesses that have secured an HCD loan within the previous 90 days.

Not located in HI, NJ, PR, MI, NV, or the Caribbean Islands.

No, you need to be a United States citizen with an SSN to qualify for a business loan through Camino Financial.

No, we cater our business loans to businesses that have established credit history.

No, we don’t require any type of collateral, only a UCC lien.

Camino Financial does not extend small business loans to businesses operating within these industries: Transportation, Warehousing, Real estate, Financial investing or processing, Cannabis industries, Adult entertainment, Car dealerships, Credit unions, and other sectors Specialty Trade Contractors require a FICO score of 650 or above. No businesses that have secured an HCD loan within the previous 90 days. Not located in HI, MI, NV, NJ, PR, MA, NY, ND, OH, PA, or TN; plus IN, NE, or WV for Sole Props.